-

Global/EN

- Global

- North America

- Latin America

The current and uncertain market environment demands vigilant analysis and adaptability in the face of short- and long-term drivers shaping the need for efficient and sustainable feed and food production. Before diving into the details of grain prices, it is important to briefly explore some key factors that are currently impacting the value chain, highlighting the level of uncertainty that is still present in the market. Let’s start with the global economy and its challenges. Although with a certain level of uncertainty, it is possible to say that the outlook for inflation and – as a result – for consumer behavior is getting more positive. In the European Union, for instance, the inflation that was above eight percent in 2022 is projected to gradually decline and register around two percent in 2025, according to the European Central Bank. Real GDP growth in Europe is also expected to gradually improve in 2024 and 2025, although at a slower-than-expected pace given the tighter monetary policy to fight inflation. Therefore, we could describe this macroeconomic driver as still uncertain, but less than it was over the last few years.

It is also important to highlight the importance and the impact of weather conditions on crops. The sector just faced very challenging seasons in South America, mainly in 2021/2022 and 2022/2023. Argentina, for instance, was extremely impacted by consecutive years of La Niña weather phenomenon, which brought a significant impact on the global availability of soymeal, given that they are its biggest exporter. For 2023/2024, even with El Niño now predominant, the forecast has become more positive in producing countries, leading to better outcomes for the grain industry. However, the risk remains present, as the season is not finished in South America. The improvement in grain availability is a key factor that leads to an improved outlook also for the animal protein value chain. In fact, grain prices have already decreased significantly over the last few quarters. While the grain sector will be explored in detail during this article, it is important to highlight that energy costs – although gradually improving – are becoming more uncertain given the conflicts in Ukraine and in the Middle East. It is also worth noting other less optimistic factors in the short term. Animal diseases, for example, are very difficult to predict. African swine fever and avian influenza are indeed key concerns in the value chain, as they can impact not only the animal protein sector but the whole value chain due to the potential disruptions in production and trade. Finally, it is important to acknowledge geopolitical trends as the most difficult to anticipate, whilst emphasizing the significant level of impact they have on our value chain.

Looking ahead to the longer-term landscape, however, we can continue to expect solid demand for grains coming from the animal protein sector: Egg production, for instance, is expected to increase by 14 million tons over the next ten years to meet global demand, just to highlight one example. This, in turn, will certainly keep demand for feedstuff growing in the next years.

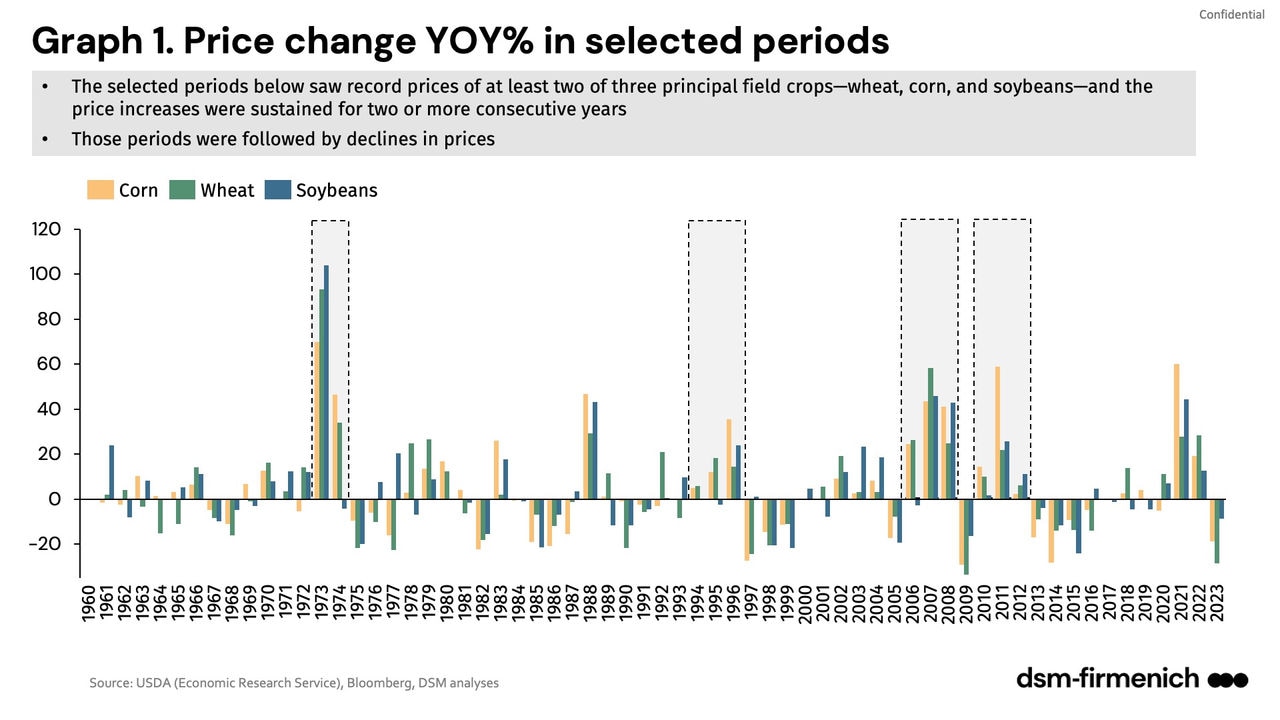

Corn, wheat, and soybean: a historic analysis, using past examples to offer insights into the future There are only four periods in the last 60 years, before 2021, which saw record prices of at least two of the three principal field crops, where the price increases were sustained for two or more consecutive years. These were: 1973-74, 1994-95, 2006-08, and 2010-12. Those periods were followed by declines in prices. Factors influencing each period mirrored many of the current uncertainties discussed earlier in this article, including weather conditions, economic change, and availability of raw material.

For example, the period of high prices during the 1970s ended with growth in global consumption slowed because of declining global economic expansion and oil prices, which reduced the availability of “petrodollars”. At the same time, global grain and oilseeds production – supported by higher prices – inclreased faster than consumption.

In other periods, higher prices supported investments in innovation and/or logistics in developing agricultural areas (e.g. South America). The gains in production coupled with the slowdown in consumption caused global stocks of grains and oilseeds to grow, pressuring prices – however it is important to mention that prices normally stabilize at “new-normal levels”, a bit higher than the previous average. The latest occasion grain prices reached these records for consecutive years was 2021-22, due to factors including COVID-19 disruptions, the Russian invasion of Ukraine, and adverse weather. So, the perfect storm made it happen again for the fifth time in the last 60 years, with two of the three main crops achieving record levels for two or more years.

Given that each of the historic periods was followed by a decline in grain prices, we can also expect more stable prices for the next few years following the most recent occurrence of record levels. In fact, like other periods, in the current situation, many market adjustments are already occurring.

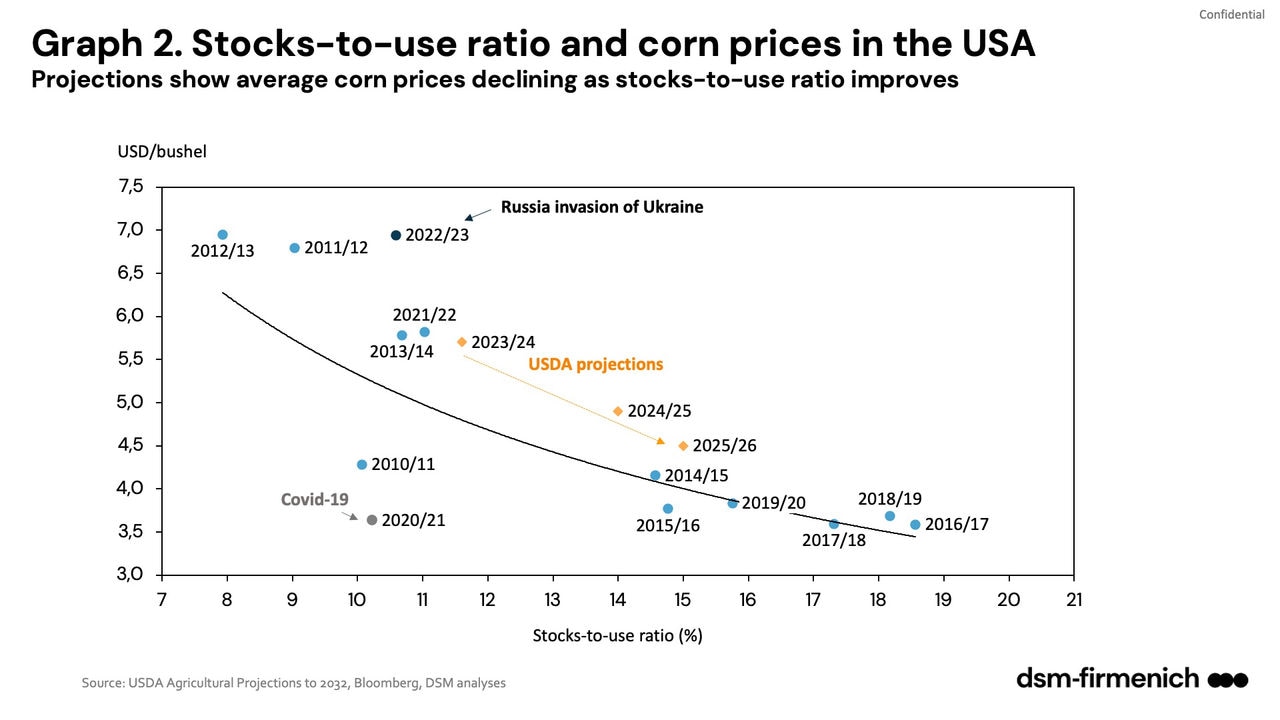

Another important indicator that supports this scenario is the correlation between stocks-to-use ratio and prices for corn, wheat, and soybean. In graph 2, it is possible to see the example of corn. Despite some outliers caused by unprecedented events such as the Russian invasion of Ukraine and COVID-19, there is a trend that prices will typically follow.

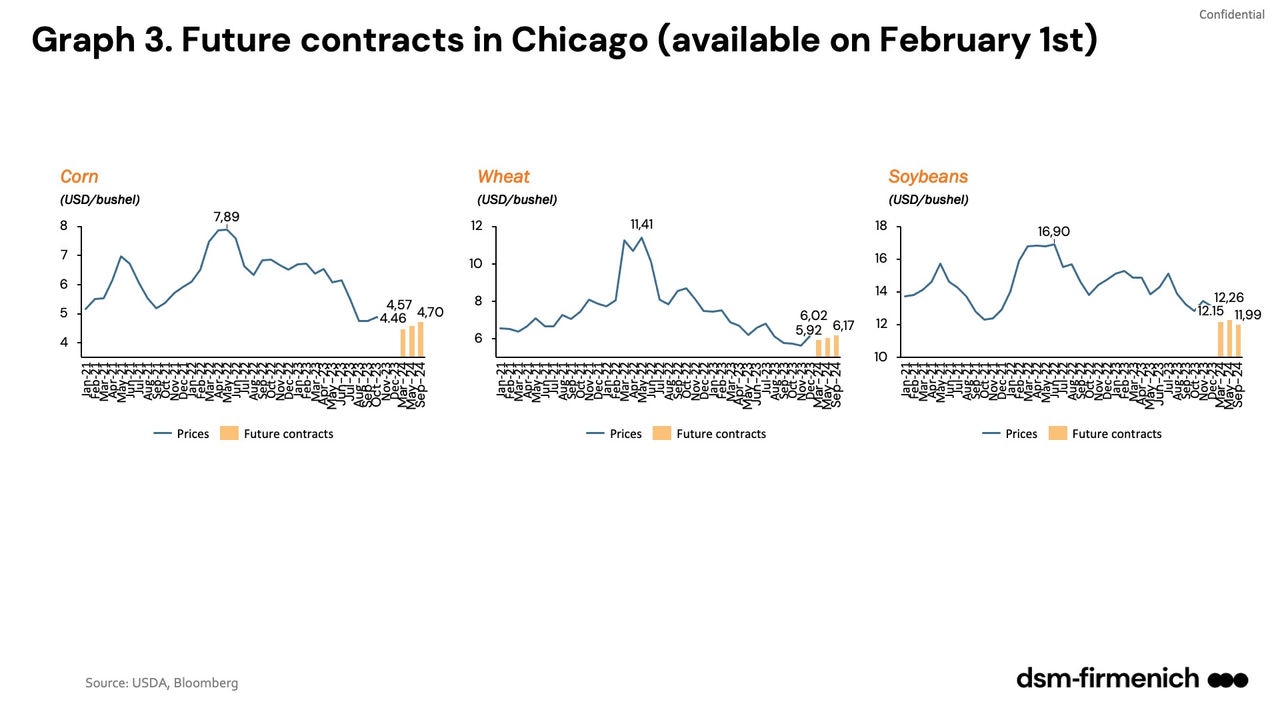

Looking at the USDA projections for the coming three seasons (available in the report: USDA Agricultural Projections to 2032), it is expected that prices will follow this trend line, but most likely with some volatility given the new market environment. Prices will probably continue to decline but stabilize at a higher level – the same as what happened in the 70s, 90s, and 2000s. While the trends are very similar for corn and wheat, with prices returning to the trend line, for soybeans the stock-to-use ratio is not projected to increase significantly over the next three years. Even so, prices are expected to return to lower levels, as is possible to observe in Chicago (see graph 3).

It is important to emphasize that the current market environment is very different from the past. In fact, the world is not becoming less uncertain. Therefore, analyzing market trends and scenarios – as explored in this article – has become a crucial exercise for companies in the food value chain. It is worth noting that some events can change a scenario overnight. While some challenges will certainly remain present in our market analyses in the near future, some long-term drivers will not disappear, such as the growing population, the consequent increase in animal protein demand, and the need to produce food in a more efficient and sustainable way. These factors will indeed keep our value chain busy working to feed the world.

15 February 2024

Adolfo holds a Master's degree in Entrepreneurship and an MBA in Economics from FEA-USP (University of São Paulo). He has 20 years of experience in market and business intelligence, with over 15 years dedicated to the agribusiness sector. He joined dsm-firmenich in 2019 and is currently Global Head of Business Intelligence for dsm-firmenich Animal Nutrition and Health.

Get in touch with a dsm-firmenich Animal Nutrition & Health specialist or find contacts around the world to suit your needs.

At dsm-firmenich, we love to connect with you.

Follow us on any of the channels below.

We detected that you are visitng this page from United States. Therefore we are redirecting you to the localized version.