-

Global/EN

- Global

- North America

- Latin America

Aquaculture is well positioned to be a sustainable provider of nutritious and affordable animal protein. In 2021, three of the top 10 animal protein companies ranked in the FAIRR index for sustainability were from the salmon farming industry, with one in the top position. So, how much progress have we made as an industry towards improving the sustainability of fish and shrimp farming? To answer the question, we must look at the basket of raw materials being used in commercial operations, since the feed accounts for the majority of cost as well as up to 80 percent of environmental footprint or emissions. From a reputational and sustainability angle, the raw materials basket has long been an area of focus, particularly when it comes to the use of fishmeal, for example. The aquaculture industry’s progress on sustainability relies on diversifying its use of marine raw materials, responsible sourcing of soy and adding novel ingredients such as algal oil, insect meal and single-cell proteins to the raw material basket. Surprisingly, in Norwegian salmon feeds, probably the front runner in sustainable thinking, less than one percent of raw materials were classified as novel in 2020 (NOFIMA, 2022).

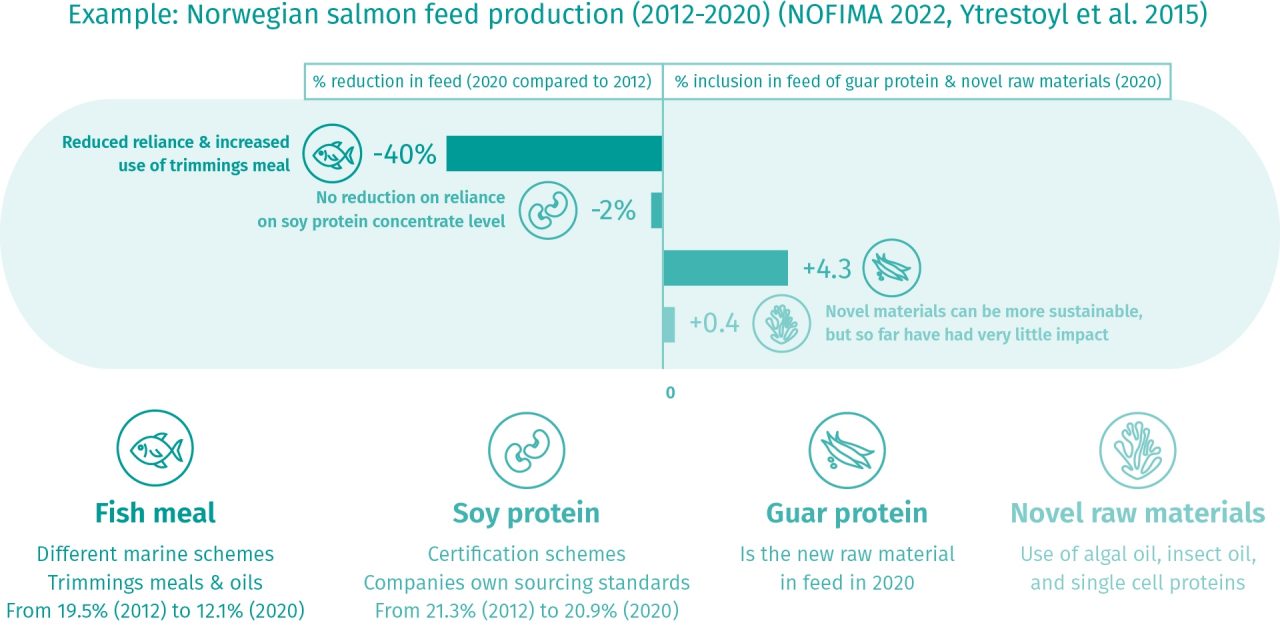

Fishmeal use dropped by 40 percent in Norwegian salmon feeds in the period 2012 to 2020 (Figure 1). If the reduced reliance on fishmeal was the only indicator of sustainability, then this would be a success story. On the other hand, some challenge the use of fishmeal at all. If we look at other raw materials, there was virtually no change in the use of soy protein concentrate (~21 percent). And in 2020, there was only guar meal that was recognised as a new raw material – at 4 percent inclusion.

Figure 1

Figure 1

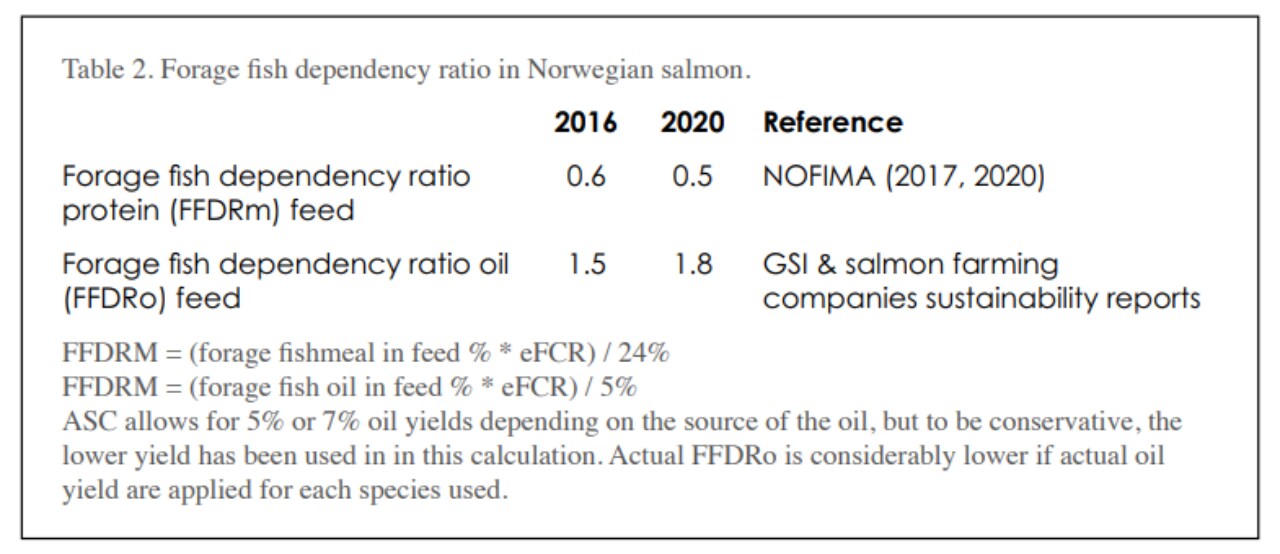

Diversifying marine raw material towards the use of waste streams with trimmings from the white fish industry as an example, has been an important strategy for the salmon feed companies, especially in Europe, where the use of animal by products is not accepted by the market. In general, approximately 30 percent of marine raw materials is sourced from trimmings in the Norwegian salmon industry (2020 company sustainability reports). The metric, forage feed dependency ratio for protein, fell to 0.5 in 2020 (from 0.6 in 2016), highlighting a reduced dependence on marine proteins (Table 2). At the same time, there was an increase in forage fish dependency ratio in oil – so the industry was adding more fish oil – related to performance, health and welfare of the fish (as well as delivering the higher omega 3 in the salmon fillet) (Table 2). Adoption of targets and commitments on sourcing of marine stocks and ensuring sourcing from sustainably managed fisheries has been evident the last years. For example, MSC and MarinTrust certified marine ingredients and adoption of fisheries improvement programs in some markets. If we look at the raw material basket for salmon feeds, it is the vegetable proteins and vegetable oils that have a large proportion of the environmental impact. Even though we hear a lot about marine proteins, the carbon footprint of the feed is not highly driven by these raw materials. When we start comparing different raw materials in terms of sustainability, we need to consider the full picture using multiple criteria and reliable data.

Table 2

Table 2

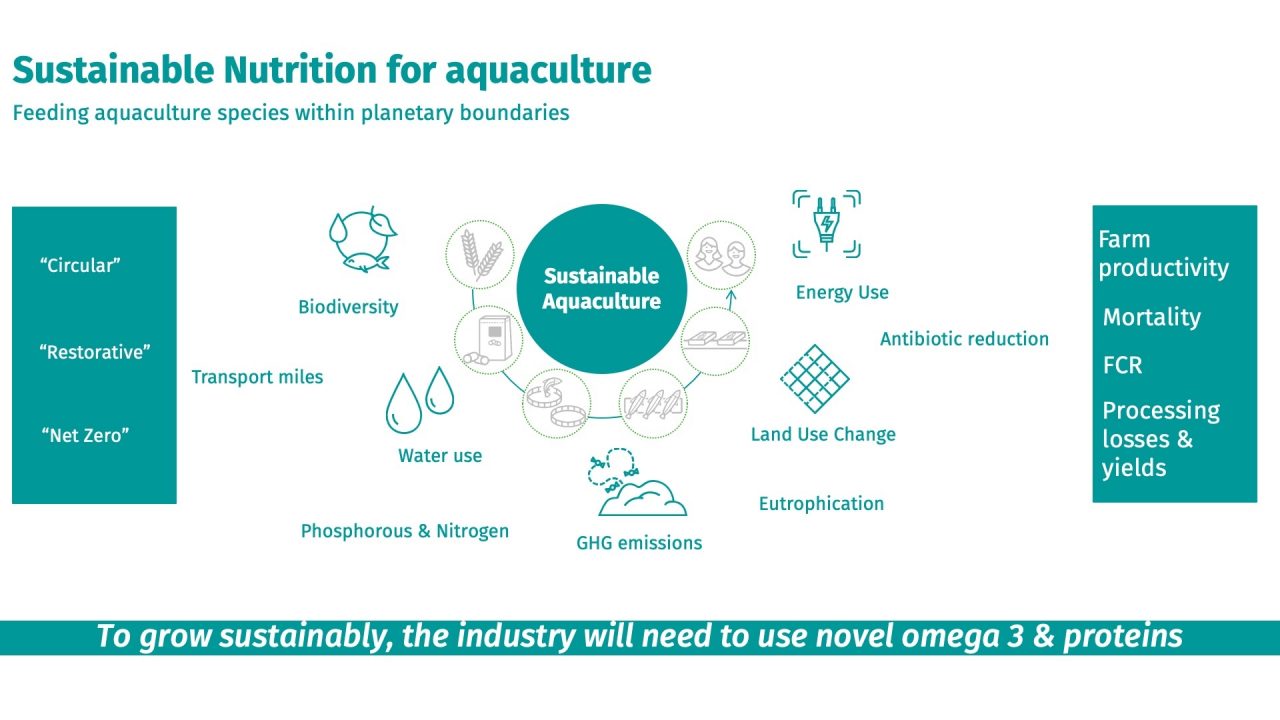

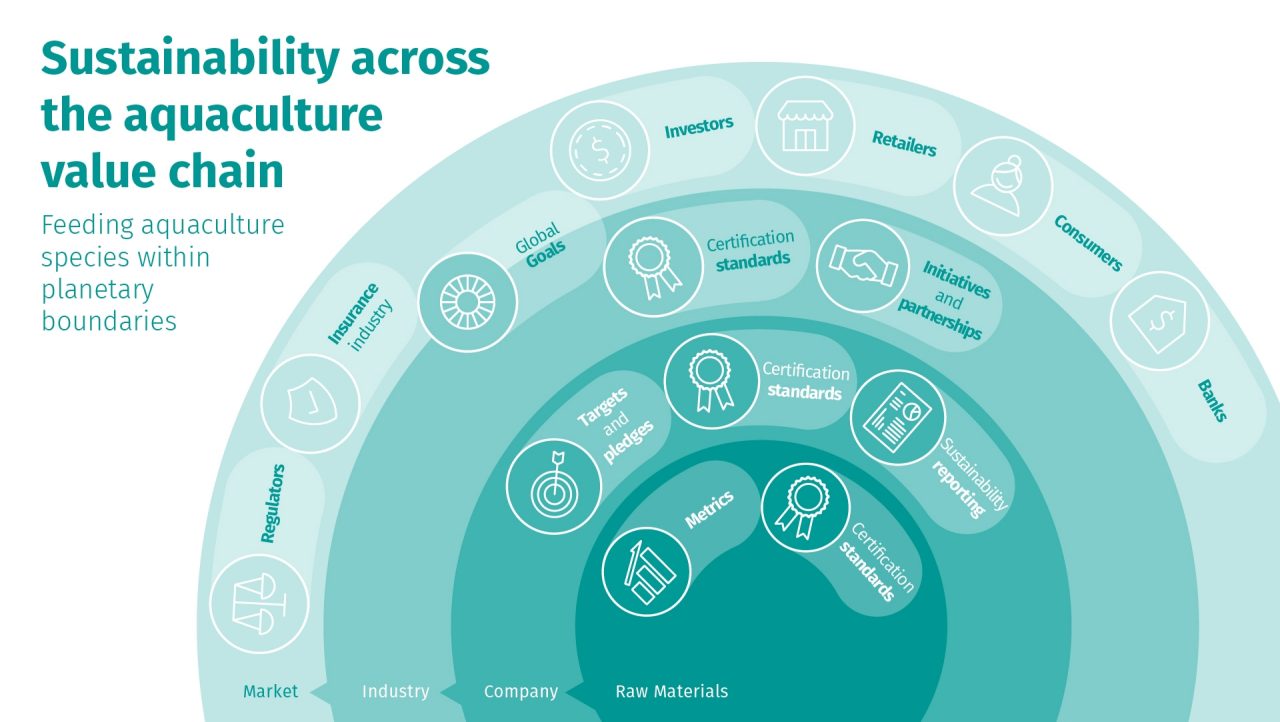

Sustainable nutrition for aquaculture can be defined as feeding aquaculture species within planetary boundaries. Around our value chain for sustainable aquaculture, we have many impacts that we need to consider – and these include biodiversity, water use, GHG emissions, antibiotic reduction (Figure 2). In addition, we have new terminology with which to learn (see Box 1). Farm productivity is the baseline to driving sustainable production and efficiency of production is key. With knowledge and investment in nutrition, feeding and husbandry practices feed conversion rates have been driven lower with time in many of the farmed species. But mortality rates in some commercial operations are not sustainable long term.

Figure 2

Figure 2

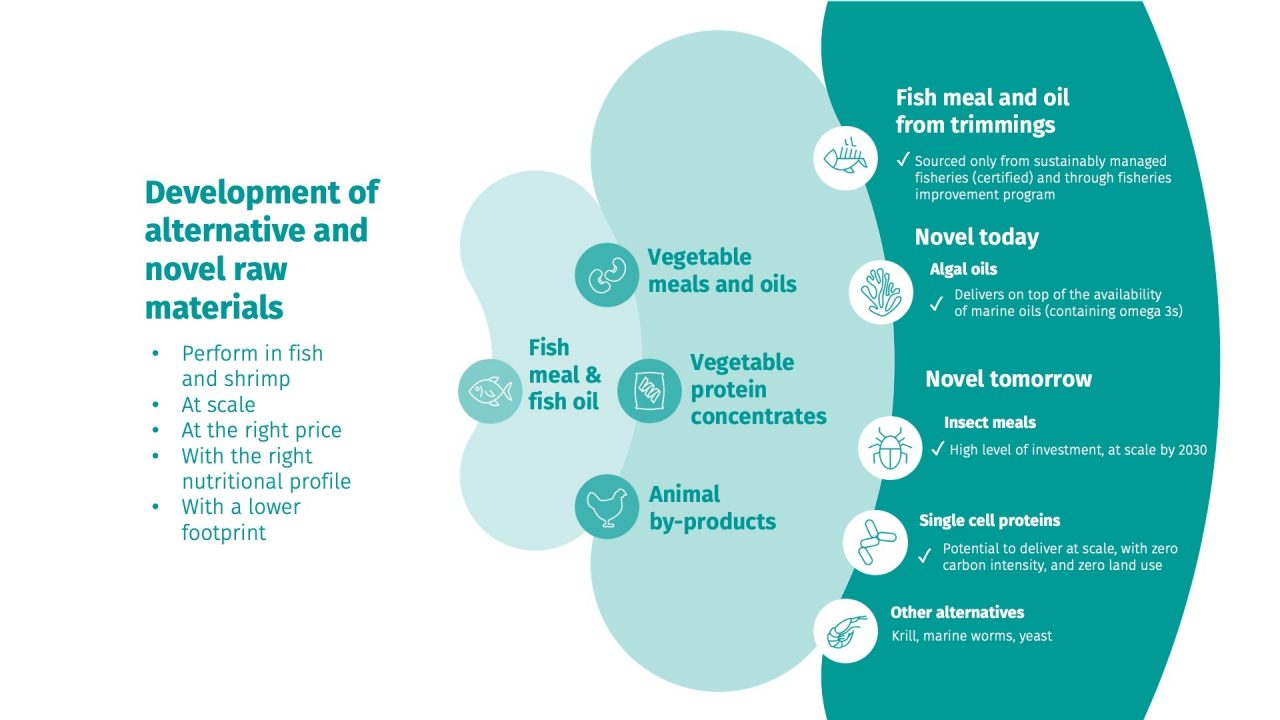

We often hear calls for the industry to develop alternative raw materials, but if we are talking large shifts in the raw materials then this means novel raw materials and not only alternatives to marine ones. The criteria being to perform in fish or shrimp, be at scale, the right price, nutritional profile and today – with a lower footprint. (Figure 4 summarises some of the options today and tomorrow.)

At the 2022 International Symposium on Fish Nutrition and Feeding, insects were the topic of many oral presentations, and insect companies have recently been a darling of capital investors. For example, there are disclosed investments in insect companies of nearly one billion Euros, and an increase in capital flow once the regulations in Europe allowed the use of insect meals in aquaculture feeds. In terms of volumes, Rabobank estimate that by 2030 the market could reach 500,000 metric tons and some of this volume would be accessed by the aquaculture industry. At the same time, the expectation is that the price of insect meal would come down to between 1500-2500 EUR/tonne – so closing the gap to a good quality fishmeal, potentially making it commercially viable for aqua producers.

Single cell proteins produced by fermentation technology have a massive potential for scalability – and especially with the focus on a shift to green energy – the potential to deliver at scale, with zero carbon intensity and with zero land use. Many companies are on the landscape for production of single cell proteins, and these are a promising novel raw material although so far not used at scale. There are also novel approaches with respect to feed stock. For example, Foods of Norway innovation centre are producing single cell proteins produced from yeast fed tree sugars.

Figure 4

Figure 4

The clear winner in novel raw materials space is so far algal oils. Veramaris and Corbion both supply commercially viable algal oil at scale today. These algal oils supplement the marine oil supply, allowing increased levels in the feed and further enable the sustainable growth of the industry. Uptake seems to be gaining momentum, with announcements from Cargill that they will include algal oils in all Norwegian feeds, partnerships announced between Atlantic Sapphire, Skretting and Veramaris, and Biomar’s production of feeds with algal oils going back several years.

To gain acceptance novel raw materials will also have to have a lower environmental footprint and comparable nutrition profile at a market acceptable price. The value chain is expecting us to measure our environmental impact and reduce it. Questions are coming from the value chain (Figure 4). From consumers, wanting to know the footprint of their product, to standards requiring at least GHG footprint calculation and the rise of labelling schemes such as Enviroscore which is based on a full lifecycle assessment (LCA) – and in many cases working towards science-based targets (SBTis) – to which many of retailers and the aquaculture companies have adopted. Financing of the industry is playing a role, investors and banks need to verify their loans and we are seeing already ESG performance requirements gaining traction. Insurance companies also need to underwrite climate-related risks. The importance of full LCA footprinting will increase from pressure along the value chain. The need to measure and benchmark both standard and novel raw material with the same metrics as companies commit to Science Based Targets and other environmental impact pledges. The industry will formulate on footprint, as well as nutrient and price. Most importantly, each company will need to measure their own footprint, as industry averages will no longer be acceptable from stakeholders. Accurate footprint measurement is essential and full life cycle assessment is becoming more important (Figure 5), and DSM has been working with leading animal protein producers to accelerate the use of LCA in their operations. Sustell™, DSM’s intelligent sustainability service, is an ISO 14040/44 assured system that combines measurement with practical, sciencebased, proven solutions to unlock the value of sustainability across livestock species and farming systems. In the future, environmental footprinting (and not just carbon) will be part of formulation and raw material benchmarking, and you will need to be using reliable metrics, so you can measure, monitor and reduce emissions.

Figure 5

Figure 5

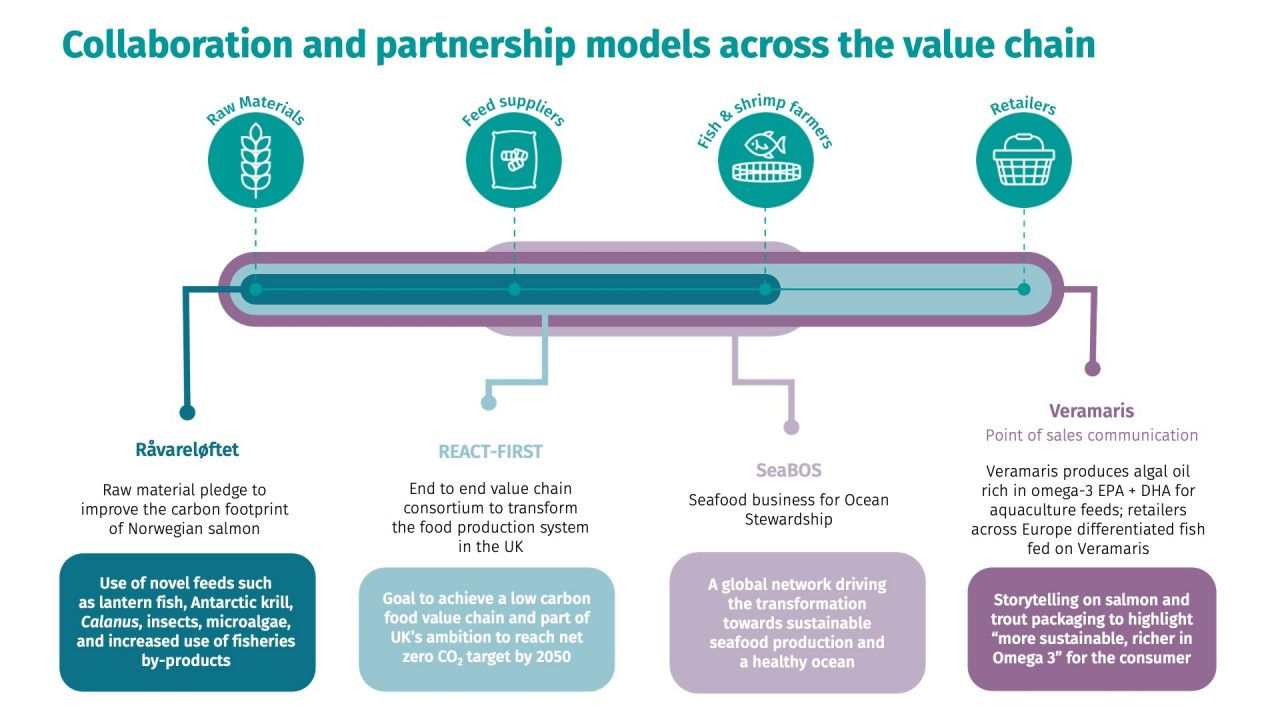

To commercialise novel ingredients, early collaboration across the value chain is key. There are some great examples of how as an industry we are mobilising our efforts and our expertise. Figure 6 shows the various configurations of partnerships and collaborations across the value chain, with raw material suppliers, feed suppliers, farmers and retailers, as well as academic bodies playing their role. The Global Salmon Initiative (GSI) caught the industry’s attention in 2015, when it led a pre-competitive invitation to tender for potential suppliers of alternative omega 3 ingredients. In addition, Veramaris has delivered a point of sales communication in several retailers across Europe: salmon and trout fed Veramaris were packaged with the information that they were raised on marine algae extracts, rich in omega 3, and preserving marine biodiversity. A successful approach to differentiation not done before in aquaculture products.

Figure 6

Figure 6

Today, there is a reduced reliance on marine proteins in aquaculture feeds, and in addition diversification of sourcing from forage fisheries alone to trimmings meals the last years, but there is still a heavy reliance on soy proteins. The industry is moving to 100 percent certification of the marine resources and soy proteins. But there are no novel proteins being used today and the technology at scale is missing (market price, volumes), even if the performance in aquaculture species is well recognised for many novel candidates and capital is not lacking (at least for insects). Today, there is gradual adoption of algae omega 3 oils, despite several options being available at commercial scale. As noted from the forage fish dependency ratios for oil, additional omega 3 sources from algae are critical to enable sustainable growth of the industry, whilst delivering salmon to the consumer with the optimum omega 3 levels. Full LCA footprinting will become more commonplace to assess and improve the sustainability of aquaculture operations. The industry is making advances at working together, and this is the only way for early adoption. However, we could also look at new business models that would be more equitable along the value chain where the commitment to pay and adoption at scale could be faster. While salmon may be the industry’s frontrunner in sustainability, many elements can be adopted to other aquaculture sectors. Part of our commitment as DSM is to facilitate the transition to more sustainable food systems. Together, with our industry partners, we make it possible.

Thanks to ISFNF for the opportunity to give the keynote lecture on which this article is based (Sorrento, June 2022).

This article originally appeared in International Aquafeed.

06 September 2022

Louise holds a PhD obtained at the University of Hull, UK. She has over two decades of industry experience in aquaculture, much of this time with EWOS and Cargill in the salmon farming countries; Scotland, Chile, and Norway. Louise held various positions in R&D, product development, innovation, and sustainability. She joined dsm-firmenich in May 2019 and is committed to delivering solutions supporting the further development of sustainable aquaculture.

We detected that you are visitng this page from United States. Therefore we are redirecting you to the localized version.