-

Global/EN

- Global

- North America

- Latin America

Farmers are increasingly recognizing the impact of climate change, prompting a growing awareness of the necessity to alleviate environmental pressures at social, political, and operational levels. The obligation to monitor and document pollutants, decrease emissions, and disclose this information is no longer exclusive to large industrial companies; it has become a crucial aspect for enhancing market standing, competitiveness, and effective communication strategies.

Historically, agricultural enterprises were exempt from these responsibilities, given the intricate nature and diversity of production of various final products. Nevertheless, it is imperative to assess how farming activities contribute to emissions, identify areas for intervention, and determine the effectiveness of chosen reduction measures, so that farmers can improve the sustainability of their operations and communicate it to their stakeholders. Accurate measurement of greenhouse gas and air pollutant emissions is essential in this process.

It is highly recommended to adopt this approach and management style as soon as possible, and to consciously assess and develop the company in line with the EU Taxonomy (BDO, 2023).

Growing public awareness of air pollution and climate change, as well as the international conventions regulating these issues, such as the Geneva Convention and the Gothenburg Protocol, the UN Framework Convention on Climate Change, the Kyoto Protocol and the Paris Agreement, have led the European Union to set a number of targets for reducing air pollutants and GHG emissions over the past decade:

For agriculture, there is no overall emission reduction target at EU level. There are agricultural policy measures offered as incentives for emission reduction, as well as requirements on downstream players (processors, abattoirs, FMCG companies and retailers) to document their sustainability efforts on e.g. GHG emissions and deforestation.

At present, the only environmental law specifically mandating responsibility for farmers, specifically those involved in intensive1 pig and poultry production, is Directive 2010/75/EU of the European Parliament and Council on industrial emissions (IED). The IED outlines both industrial activities and corresponding capacity thresholds that require environmental permits. Operators are obligated to prevent and minimize pollution of air, water, and soil in a comprehensive manner. To meet these goals, the legislation requires the use of Best Available Techniques (BAT) and the monitoring of emissions as outlined in BAT reference documents. However, for pig and poultry production, emission monitoring only encompasses nitrogen and phosphorus excretion, as well as ammonia emissions, and so far does not address GHGs.

1Intensive rearing of pigs or poultry: more than 2,000 places for fattening pigs (over 30 kg) or more than 750 places for breeding sows; more than 40,000 places for poultry.

Environmental awareness and sustainability have become expectations for companies. Therefore, decarbonisation is strategically focused on by many firms and there is growing demand to work with more sustainable suppliers. Environmental product labelling has become a key tool to promote consumer awareness in developed countries (Moran and Wall, 2011). An increasing number of companies in EU member states are initiating sustainability campaigns, promoting their environmentally-friendly innovations, and pledging to achieve carbon neutrality within a few decades, namely by making commitments to the Science Based Targets initiative.

Carbon accounting enables organisations to respond to increasing pressure from regulators, customers and investors to report and reduce emissions. At the same time, new regulations as part of the European Green Deal require companies to account for their resource use and carbon footprint across their entire value chain. Monitoring and reducing GHG emissions from agriculture is swiftly becoming a key priority for many food and beverage firms. Fortunately, methodologies and databases are becoming available to help farmers get a clear picture of the environmental footprint of feed and animal protein.

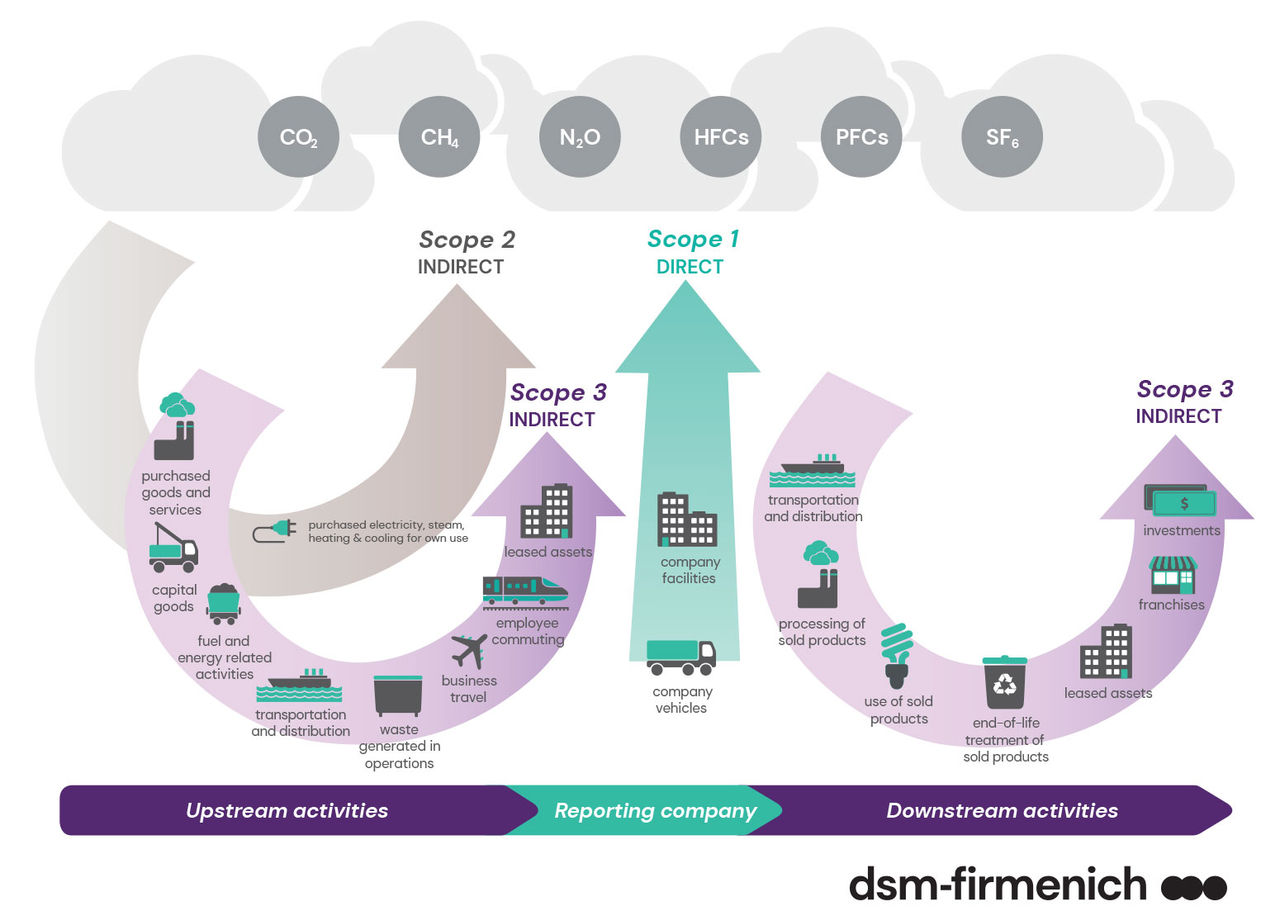

With the development of corporate sustainability and social responsibility in the late 2010s, an ESG (Environmental, Social & Governance) reporting framework has been established to facilitate business investment decisions. The objective of this framework is to understand and measure the sustainable performance of companies and to monitor non-financial opportunities and risks. It includes the need to account for corporate GHG emissions, which are commonly measured using the GHG Protocol, the prevailing international standard. The standard classifies the emissions associated with the operation of a company into direct and indirect categories and defines the scope of emissions accounting as follows:

Figure 1: Overview of GHG Protocol scopes and emissions across the value chain | Source: GHG Protocol, 2011

Figure 1: Overview of GHG Protocol scopes and emissions across the value chain | Source: GHG Protocol, 2011

The GHG Protocol offers four different accounting approaches for determining the carbon footprint, which companies can choose from. The approaches vary considerably in their degree of complexity. However, such freedom allows companies too much room for manoeuvre, ultimately compromising the credibility and comparability of the accounts.

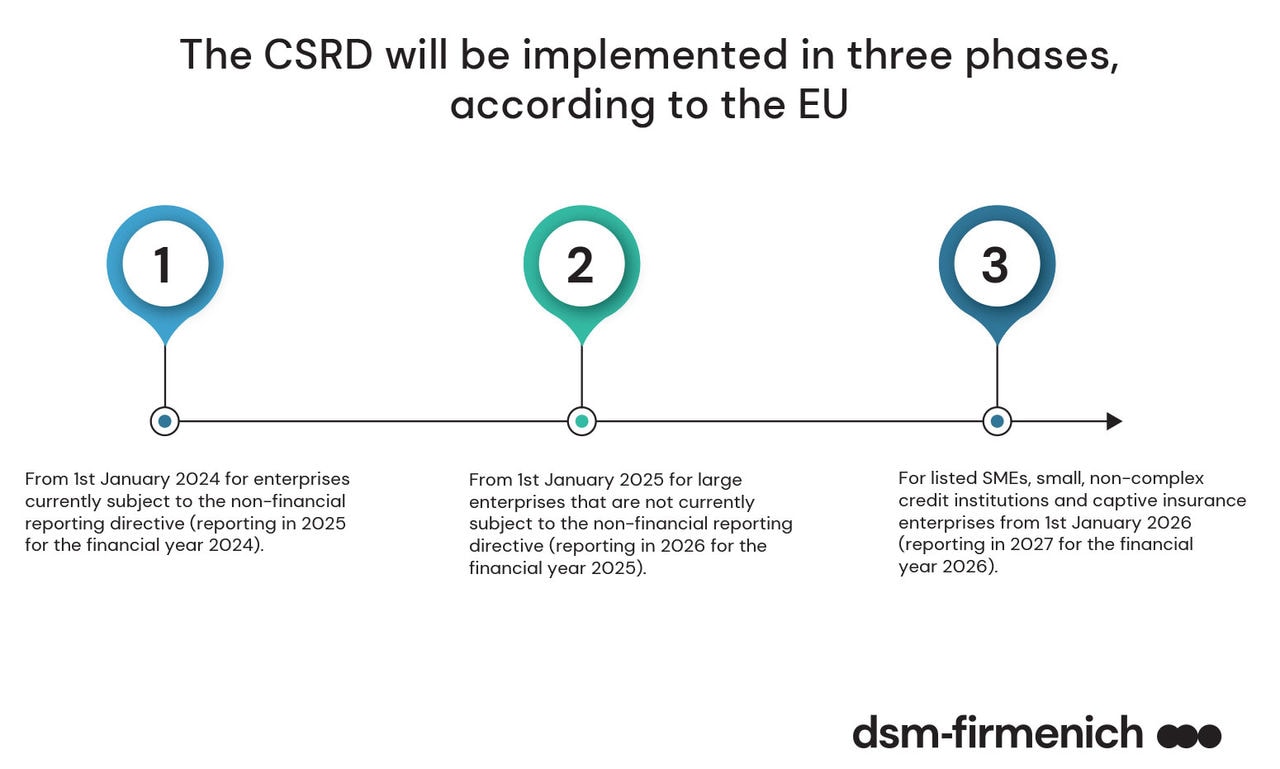

In order to ensure a credible, complete and comparable carbon footprint, the European Parliament adopted the Corporate Sustainability Reporting Directive (CSRD) in November 2022 to support the actions of the European Green Deal. This significantly extends the scope of the current Non-Financial Reporting Directive (NFRD). The European Sustainability Reporting Standards (ESRS), which will be introduced as part of the CSRD, will require both large and small companies to report fully on their carbon footprint. The obligation will come into force progressively from 2024 for the different companies covered by the CSRD (Figure 2). The accounting is expected to take into account not only the direct emissions of the business, but also the carbon generated upstream and downstream, i.e. during transport, processes and use - the Scope 3 emissions. Therefore, if an agricultural business is part of a reporting company's value chain, it must account for its own emissions, even if the agricultural business itself is not covered by the Directive.

Figure 2: Phases of implementing EU CSRD. | Source: Rajpal, 2023

Figure 2: Phases of implementing EU CSRD. | Source: Rajpal, 2023

In addition to the above, pig and poultry enterprises covered by the IED must also report their annual ammonia emissions to the European Pollutant Release and Transfer Register (E-PRTR). The data reported here are publicly available. Since February 2021, farms must also annually monitor the amount of nitrogen and phosphorus excreted per animal place and the amount of ammonia emissions to air from animal houses.

The question is what methodology should be used to make these calculations, and whether software or calculators are available to support the calculations. The EMEP/EEA air pollutant emission inventory guidebook, which was published by the European Monitoring and Evaluation Programme and the European Environment Agency (EMEP/EEA), provides the methodology. However, the number of available calculators is already much lower than for carbon footprint accounting, as ammonia accounting has a much shorter history and reporting is limited to a small number of companies.

The issue of resource requirements for emission accounting arises here. Financial and human resources required for this task are more readily available to larger companies while smaller ones need an easily accessible, low-cost accounting solution. Although a variety of free-to-use business farm carbon calculators are available in the market, most of them are only carbon footprint calculators and cannot accurately track CO2 and NH3 emissions from agricultural businesses. However, Sustell™, was specifically tailored for livestock farms to address the existing challenges.

The Sustell™ platform developed by dsm-firmenich, certified through numerous certification schemes and standards, provides ISO-guaranteed full Life Cycle Analysis (LCA) for livestock farms and feed manufacturers. It enables the measurement and validation of environmental impacts, the assessment of scenarios, and the identification and improvement of key factors that influence the environmental footprint of stakeholders in the livestock value chain. The system takes a comprehensive ecosystem approach: the animal feed module deals with the environmental effects of producing and transporting feed materials, as well as the environmental effects of cultivating/producing each feed material. The farm module accounts for livestock production and manure management.

In the upcoming articles, we will employ the Sustell™ results for a selected Hungarian pig, poultry, and cattle farm to demonstrate how information can aid livestock farmers in mitigating air pollution.

24 April 2024

Her main focus areas include protein crops, with a specific focus on soybean production and its economic aspects; animal nutrition and husbandry, with a particular emphasis on sustainability, including the reduction of greenhouse gases and air pollutants; and the evaluation of the suitability of smart technologies in pig and poultry production in Hungary. These endeavours aim to provide support for decision-making processes in relevant policy areas and enhance the awareness of market participants.

Her main focus areas include national-level feed monitoring, assessing the environmental aspects of farm livestock feeding to support policy-making and the feed industry, and promoting the adoption of sustainable production systems, with a particular emphasis on transferring knowledge related to environmental pollution mitigating technologies.

Richard received his PhD in Animal feeding from the University of West Hungary, Faculty of Agricultural and Food Sciences. He joined dsm-firmenich in 2020.

He contributed to the business by working on digital strategy and by introducing Precision Service tools in Central Eastern European markets.

Get in touch with a dsm-firmenich Animal Nutrition & Health specialist or find contacts around the world to suit your needs.

At dsm-firmenich, we love to connect with you.

Follow us on any of the channels below.

We detected that you are visitng this page from United States. Therefore we are redirecting you to the localized version.